Spectroscopy: Enduring During Uncertain Times

The spectroscopy market and its major segments: atomic spectroscopy, molecular spectroscopy, and mass spectrometry, are forecasted and analyzed for the coming year.

The spectroscopy market and its major segments: atomic spectroscopy, molecular spectroscopy, and mass spectrometry, are forecasted and analyzed for the coming year. Despite a difficult business environment, the expectation is that spectroscopy demand will hold up nicely.

The analytical and life science instrument industry, of which spectroscopy is a key component, is an important resource for dealing with global challenges of ever-increasing magnitude. Overall industry growth has been in the 6–8% range now for the last few years, which is a sign of its maturity and stability. The demands of the life science marketplace, environmental concerns, the search for new materials, and security and defense concerns are important driving forces. The regional focus has shifted to developing countries, especially in Asia where growth far outpaces that of North America, Europe, and Japan. But even as application requirements evolve and markets ebb and flow, 2009 is shaping up as a major challenge for every industry including the laboratory instrument industry, and indeed the spectroscopy segment as well. The global economic recession we are experiencing is without precedent in living memory, and the uncertainty about how this will resolve is equally high.

Figure 1

Not a day goes by without more bad news, whether it be the financial meltdown, bankruptcies, growing unemployment, a slowdown in global trade, and the gloom surrounding global stock exchanges. We are clearly in the midst of a global recession that cannot be easily dismissed. Still, we are seeing unprecedented government intervention throughout the world to stem the tide of decline. Stimulus programs in the U.S., EU, Japan, China, and many other countries are bound to moderate the economic problems, as does the fact that interest rates are at extremely low levels, which should at some point encourage consumption and investment.

With these developments in mind, and after examining any and all indications of industry activity in 2008 and the prospects for 2009, Instrument Business Outlook (IBO), a publication of Strategic Directions International, Inc. (SDi), a consulting and market intelligence firm specializing in this market, has estimated the total worldwide market for analytical and life science instrumentation and related aftermarket and service revenues at about $38 billion for 2008. This represented an overall increase in industry revenues of about 5.3% from 2007, which was less than expected because of the global economic slowdown that surfaced in the last three months of 2008. SDi forecasts the analytical and life science instrument industry growth to moderate further in 2009 and to expand at the rate of 4.8%. While not particularly exciting, it is a level of expansion that would be very welcome in many sectors of the global economy and not nearly the gloomy overlook that some analysts have predicted for the industry. That said, it is apparent that even this resilient business is being affected by the worsening global recession.

Figure 2

Some instrumental techniques will, however, suffer more as the primary industries they serve cut back, including metals and mining, petroleum and chemical processing, and of course, semiconductor and electronics. On the other hand, those techniques that deal with the life sciences (pharmaceuticals, biotechnology, and food and agriculture testing) will weather the storm quite nicely. Likewise, some regions of the world, like China and India, will continue to offer growth potential, but at a somewhat less robust level. We do, however, expect the first half of 2009 to be a very difficult time for the industry in general, but the second half will pick up briskly as the recession winds down and the stimulus kicks in.

The pace of global mergers and acquisitions slowed somewhat in 2008. However, several deals of significance did take place, especially one blockbuster transaction. Invitrogen acquired Applied Biosystems in November 2008 and quickly changed the name of the new organization to Life Technologies Corporation. The newly designated company is a powerhouse in life science technologies and includes various instrumental techniques such as Real-Tine PCR, DNA sequencers, and mass spectrometers, as well as a plethora of reagents and kits for molecular biology and cell analysis. General Electric continued in its acquisitive mode by purchasing Whatman, a major filtration supplier, in February 2008. Agilent Technologies, Inc. expanded its involvement in the material science arena by acquiring four firms representing a variety of new techniques for materials characterization. Qiagen also acquired two firms, Corbett Life Sciences and Biotage's Biosystems business, giving it thermal cycling and sequencing technologies, which are among the fastest growing life science markets.

Figure 3

Interest in aftermarket products and services, including such items as consumables (especially chemicals), software updates, and accessories, is keener than ever. As the installed base of instruments grows and the market matures, the aftermarket becomes especially important. In fact, in selected technology areas, the aftermarket is a very significant product segment that is growing faster than instrument system revenues and is often more profitable. It is also true that for some technologies, instrument systems (hardware) might actually be declining in unit sales while the aftermarket provides at least minimal growth. So it should be noted that all the revenue projections in this article include the total mix of revenue sources: instrument system sales, aftermarket, and service.

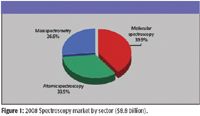

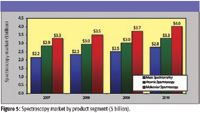

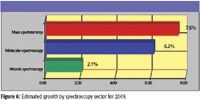

The spectroscopy market can be segmented into three distinct sectors: molecular spectroscopy, atomic spectroscopy, and mass spectrometry (MS). The applications of the techniques included in each sector and their prospects differ significantly, especially within each sector. Worldwide revenues for all spectroscopy segments is estimated at $8.8 billion for 2008, or about 23% of the entire laboratory analytical and life science instrument market. The overall spectroscopy market is estimated to have grown 5.8% in 2008, a significantly lower level than what was predicted last year. SDi projects spectroscopy market growth in 2009 to be moderately lower than for 2008, increasing at about 5.2%. This is a function of the fact that some of the growth markets have cooled off and because of the now-realized global economic slowdown. Still, the spectroscopy market is projected to grow faster than the remainder of the laboratory instrument market, which is a continuation of the pattern for the last several years.

Figure 4

Molecular spectroscopy techniques account for almost 40% of the spectroscopy market, although many diverse techniques are represented that address a wide range of applications in almost every industry category. Atomic spectroscopy is the second largest sector at over 33%, while MS approaches 27% of spectroscopy revenues. Please note that liquid chromatography (LC) and gas chromatography (GC) front-ends to mass spectrometers, and their associated aftermarket and service revenues, are not included in this analysis.

Molecular Spectroscopy

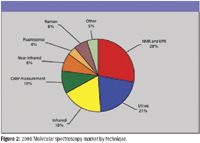

The market for molecular spectroscopy is estimated to have exceeded $3.5 billion in 2008. Overall, the total revenues for all categories of molecular spectroscopy grew 6.3% last year. However, growth rates differ measurably for the various instrumental techniques, led by the continuing success of the nuclear magnetic resonance (NMR) segment, while fluorescence spectroscopy has experienced the slowest growth. No single technique dominates this market, although the NMR and UV–vis product segments account for almost 50% of the overall molecular spectroscopy market.

Growth in the overall molecular spectroscopy market is expected to remain much the same for 2009 as that experienced in 2008, despite the global recession. With the exception of color measurement and ellipsometry, most other molecular spectroscopy instrumentation techniques are significantly focused on selected industries that are seen as being largely insulated from the current economic crisis, namely healthcare, government, and academia.

Figure 5

The consistently solid growth of the vibrational spectroscopy methods, which include Raman, infrared (IR), and near-infrared (NIR), is in large part due to the rapid rise of portable handheld molecular spectroscopy instruments. The technological advancements made during the telecommunications revolution of the late 1990s made possible much more compact, reliable, and robust instruments that required less power. When combined with major advancements in battery technology, the result was a slew of new handheld spectroscopy instruments. Much of the new demand for these products is coming from various government entities for defense, domestic security, and first-responder usage, as well as from environmental applications. The quality and performance of many of these handheld instruments also rival that of lower-end benchtop systems, which will tend to cannibalize a significant portion of those market subsegments. Both IR and NIR are expected to expand in the 6–7% range for 2009. Demand for Raman spectroscopy has now reached quite sizable proportions, and the technique will continue to see strong double-digit growth in the near term.

The two weak areas in the molecular spectroscopy market are color measurement and ellipsometry. Much of the demand for color measurement comes from the textiles and automotive industries, which have collapsed in 2008, and are likely to continue downward in 2009, taking demand for color analysis instrumentation with them. By far the largest demand for ellipsometry comes from the semiconductor and electronics industry. Although some segments of this industry are doing well, such as photovoltaic cells for solar arrays, most of the industry is considerably depressed, and is not likely to pick up any time soon.

The NMR market, which is by far the largest segment of the molecular spectroscopy market at over $1 billion, will see slightly slower growth in 2009, but still in the high single digits. The extremely high cost of higher-end NMR initial systems has caused many end-users to pause and reconsider such large capital expenditures in the current economic environment. However, nearly a third of demand comes from academic and government research laboratories, which are somewhat insulated from the wider economy. The other factor helping to maintain consistent demand in the NMR market is the installed base, and the considerable amount of service and aftermarket products, such as probes and cryogenic gases, that are required to maintain and operate such systems.

Figure 6

Like other molecular spectroscopy markets, growth in demand for UV–vis and polarimeters and refractometers will be down slightly, but not dramatically. Most of the instruments in both of these areas are relatively low in cost, priced between a few hundred and a few thousand dollars. Therefore, such purchases are not highly dependent on major capital expenditure decisions by end-user organizations. The UV–vis market is also benefiting from the rapid increase in demand for microvolume instruments, which are heavily tied to the biotechnology and hospital–clinical industries.

Fluorescence instrumentation is also tied to the life science market, but standalone instruments continue to exhibit sluggish demand. This is primarily because of microplate readers that often include a fluorescence detection mode and offer productivity improvement potential for many applications.

A very large number of suppliers participate in the molecular spectroscopy market; however, overall market share positions tend to be a function of dominance in particular product segments. Bruker is the overall leader based on its very significant NMR and electron paramagnetic resonance (EPR) business as well as its involvement in infrared technology. Varian is also a major NMR vendor with a leading role in UV–vis. Thermo Scientific and PerkinElmer, in the third and fourth positions, offer a wider array of molecular spectroscopy instruments, but with very strong positions in infrared and UV–vis. X-Rite holds the number five position based on its dominance in color measurement.

Table I: Spectroscopy product growth prospects for 2009

Atomic Spectroscopy

The market for atomic spectroscopy instruments is expected to slow measurably in 2009 and expand at just 2.1%, a significantly lower level than has been seen the last few years. However, within this $3 billion market, growth varies widely for the techniques included. During the last two to three years, market demand for atomic spectroscopy instrumentation has especially benefited from the increased global demand for minerals and metals and their concomitant high prices, as well as by recently enacted environmental regulations. This continued until mid-summer 2008, when the air went out of the mineral and metals balloon.

Many atomic spectroscopy techniques are well suited for the analysis of trace elements in water and other sample types; consequently, they have a strong environmental focus. Because a large portion of environmental testing is mandated by regulations, these applications should be fairly insulated from the negative effects of the global economy. The continuing international interest in green technologies and environmental safety should also remain strong sources of growth in demand for atomic spectroscopy. The techniques most associated with environmental testing are atomic absorbance (AA), inductively coupled plasma (ICP) spectroscopy, ICP mass spectrometry (ICP-MS), and the various elemental analysis techniques. Traditionally, these techniques grow at single-digit rates and this will be true in 2009 as well, although the rates will favor the lower end of that range. Of these, ICP will experience the least growth, remaining virtually flat over 2009. The fastest growing segment is in elemental analysis, where total organic carbon (TOC) continues to expand its reach into industrial markets and other types of water analysis. Organic elemental analyzers will see above-average growth, exceeding 5%, because of their focus on food and agriculture, while the inorganic analyzer market, a technology area closely associated with metals analysis, will expand at a slower rate. The exception here is mercury analysis, which is still very much in demand.

On the other hand, some atomic spectroscopy technologies can expect to be affected more severely by the global economic downturn. Production of metals is likely to diminish in the short term. This will not only affect steel production for products like automobiles, but other metals as well, such as aluminum. Arc-spark spectroscopy is strongly tied to metal production, and this market is forecast to fall as much as 9% in 2009. X-ray fluorescence (XRF) and (to a lesser extent) X-ray diffraction (XRD) also have strong ties to metals and mining, but these technologies have important applications in other areas that should moderate the negative effects. Nevertheless, although the X-ray technologies have recently grown at double-digit rates, the forecast for 2009 will fall well short of 10%. Indeed, XRF will not grow much at all in 2009, though this may reflect more on how good a year 2008 was for XRF. Handheld XRF has enjoyed enormous growth as it expanded the technology into new markets, but even in 2008 it was already becoming more difficult to find new areas into which to expand. In contrast, XRD should continue to receive support from academic and government spending, making the technology the category growth leader at 7.5%. Although arc-spark will suffer a significant decline, it is the smallest market. With most of the other technologies posting minimal gains, the overall market is still forecast to grow at 2.1% in 2009, buoyed primarily by XRD and elemental analysis.

The total atomic spectroscopy market is fairly consolidated, with the top five vendors combining to make up nearly half of the market. There has been a recent trend among the suppliers of X-ray instrumentation to pursue acquisitions or other business relationships in related areas of spectroscopy, primarily arc-spark. For instance, Bruker has acquired Quantron (arc-spark) and JUWE (elemental analysis), Oxford Instruments acquired WAS (arc-spark), and PANalytical (Spectris) has formed a close relationship with OBLF (arc-spark).

Spectris, Bruker, and Rigaku, which all participate primarily in X-ray spectroscopy, hold the third through fifth spots in overall vendor share. In second place, PerkinElmer relies on its dominance in the more environmentally focused technologies: AA, ICP, and ICP-MS. Thermo Scientific is the leading atomic spectroscopy supplier. Thermo competes in all of the individual technology areas within atomic spectroscopy, a distinction it shares only with Shimadzu. More focused players dominate in some markets. The prime examples would be Spectro Analytical (AMETEK), which leads the arc-spark market, and LECO, which rules the field of elemental analysis.

Mass Spectrometry

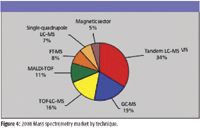

It should be no surprise that the MS market once again is the growth leader in spectroscopy. The unique capabilities and technical performance of various MS products helps to drive demand for these instruments, especially for the increasingly challenging analytical applications in today's modern laboratory. The worldwide market for MS easily passed the $2.3 billion mark in 2008 as revenue growth exceeded 8%. Despite the severe global recession, SDi expects the demand for MS to grow at 7.6%, which will easily put the total market over the $2.5 billion mark. The fact that more than two-thirds of the MS market is closely connected with government, academia, and the healthcare industries is the primary factor for its demand resiliency. A stream of new product introductions advances the limits of performance and is a major factor for the support that this technology is given by scientists throughout the world.

There has been a softening in demand for initial systems, especially for the more expensive systems that can cost over half a million dollars. New orders for initial systems are either being delayed or put on hold, rather than cancelled outright, as end-users are simply becoming more cautious in the current economic environment. MS plays an important role in certain industries such as pharmaceuticals, biotechnology, environmental testing, and increasing clinical applications, which exhibit a continuing requirement for ever-increasing sensitivity, resolution, and speed of analysis. This often trumps the demands of applications when it comes to resource allocations and capital equipment investment. The fairly large installed base and strong continued growth of the past years suggests very consistent growth in aftermarket and service demand for MS.

One market segment that is likely to be somewhat more affected by the general economic downturn is GC–MS, which is significantly associated with the oil and gas industry and petrochemical manufacturing. The price of oil has plummeted during the past few months and diminished some of the attraction of that market. The chemicals industry is likewise confronted with reduced global demand of its products, and capital budgets have been reduced drastically. However, food safety issues and environmental regulations will help GC–MS maintain at least a moderate level of growth for 2009.

The once high-flying matrix assisted laser desorption ionization (MALDI)-TOF market has experienced less than stellar growth in recent years because of a lack of product innovation. Market growth of below 4% is anticipated for 2009. While initial systems demand has been soft, one bright spot is the interest in the technology that has been stimulated by the development of a wide range of sample preparation and other aftermarket products.

Both tandem LC–MS and TOF LC–MS flirted with growth in the 9–10% range for 2008. For 2009, growth will be off a bit, but still robust at around 9% because of the present economic conditions. Another factor contributing to slightly lower growth is the availability of significantly lower priced initial system models of triple-quadrupole and quadrupole TOF instruments, which has reduced average selling prices while maintaining growth in unit sales. Continuing innovation and new product introductions in these two segments of the market will help drive market demand for the next several years. Food safety issues have also helped to stimulate demand for this segment of the market, particularly for triple-quadrupole LC–MS. Because food safety is driven much more by regulatory factors, it is also likely to be less affected by recessionary pressures.

The Fourier transform (FT)-MS market is in major flux at the moment due to the introduction of much simpler and lower cost instrument models that fall into the category, principally from Thermo Scientific. These newer systems are priced well under $500,000 and are selling very well, which is in contrast to the much larger, and much more expensive, research systems that can cost over $1 million. Although these higher-end FT-MS systems are still in demand, their low volume and high cost means that only a handful of delayed or cancelled orders could significantly affect market forecasts. Despite these factors, FT-MS will lead the MS market in terms of growth, which will clearly be in double digits.

There has been a high degree of industry consolidation during the last several years, and now five firms account for almost 80% of the MS market. Applied Biosystems, now part of Life Technologies, is the market leader, followed by Thermo Scientific, Agilent Technologies, Waters, and Bruker, all of which offer a number of MS techniques. Competition among these suppliers has intensified, as has the competition between various technologies.

The Spectroscopy Market Is Positioned to Weather the Storm

There is no question but that the diversity and scope of spectroscopy contributes to its continued importance and presence in laboratories around the world. Its utility has even moved beyond the laboratory due to the advent of innovative handheld instruments for analytical challenges that cannot easily be addressed in a laboratory. This was most evident in handheld XRF instruments that have been used to reduce lead contamination of waste disposal sites and nearby groundwater and to detect the presence of lead in toys, and most recently, to comply with new regulations in the U.S. relating to lead in children's clothing. In addition, a host of new handheld instruments based on IR, NIR, UV-vis, and Raman technologies are sweeping the market for security and defense, drug identification, food inspection, and environmental monitoring.

Atomic spectroscopy techniques are most closely associated with environmental applications and the analysis of metals and minerals, which until mid-2008 were all important sources of growth. The global economic slowdown has impacted this portion of the spectroscopy market the most, but it has not been a knockout punch. Water quality concerns still drive demand for ICP-MS and TOC and provide some support to the more mature AA and ICP markets. Likewise, XRD continues to benefit from its indispensable service in drug development. And while the metals and semiconductor industries might be disappointing this year for arc-spark and X-ray instrument suppliers, a return to stronger growth is perhaps only one or two years away.

So while the last few years have been an elemental analysis heyday, today it is a molecular world. Obviously, this change is a welcome trend by molecular spectroscopy and MS vendors alike. Drug development, cell analysis, food testing, and pesticide analysis all depend on molecular analysis technologies, and the demand today is indeed a good counterweight to the less exciting prospects for atomic spectroscopy.

Internationally, China, India, and other Asian countries, excepting Japan, is where the growth can be expected, although somewhat muted as compared with the growth of the last few years. China's export engine is beginning to sputter as its global customers struggle through their economic doldrums, so it is likely that China will focus more attention inward. What is important is that the demand in China and surrounding countries will still outpace that in developed countries, and of course, the Chinese market is no longer tiny. It will remain a significant market for the full range of spectroscopy technologies, even those like arc-spark and AA, which have dimmer prospects in North America and Europe. Likewise, India will continue to be a growth market for technologies that support its expanding pharmaceutical and biotechnology industries. Many pharmaceutical companies are relocating operations to India to join its large domestic industry. India was once a market known only for generic drug production, but now it is becoming a location for new drug development as well. China has also made progress in these activities.

Although the current economic environment is somewhat depressing, we believe that improvements are on the horizon. We also feel that the utility of the vast range of spectroscopy technologies offers the kind of diversification that is needed in an uncertain world. Because of technical developments and product innovation, spectroscopy suppliers can be expected to continue to offer attractive analytical solutions to challenges new and old today and in the years to come.

Lawrence S. Schmid is President and Chief Executive Officer of Strategic Directions International, Inc. For more information on Instrument Business Outlook or other instrumentation research, contact Strategic Directions International, Inc., 6242 Westchester Parkway, Suite 100, Los Angeles, CA 90045, (310) 641-4982, fax; (310) 641-8851, e-mail: sdi@strategic-directions.com

LIBS Illuminates the Hidden Health Risks of Indoor Welding and Soldering

April 23rd 2025A new dual-spectroscopy approach reveals real-time pollution threats in indoor workspaces. Chinese researchers have pioneered the use of laser-induced breakdown spectroscopy (LIBS) and aerosol mass spectrometry to uncover and monitor harmful heavy metal and dust emissions from soldering and welding in real-time. These complementary tools offer a fast, accurate means to evaluate air quality threats in industrial and indoor environments—where people spend most of their time.

NIR Spectroscopy Explored as Sustainable Approach to Detecting Bovine Mastitis

April 23rd 2025A new study published in Applied Food Research demonstrates that near-infrared spectroscopy (NIRS) can effectively detect subclinical bovine mastitis in milk, offering a fast, non-invasive method to guide targeted antibiotic treatment and support sustainable dairy practices.