Spectroscopy Market Slows to a Crawl

How the core spectroscopy techniques - molecular, atomic, and mass spectrometry - will fare in 2013 based on the results from last year's data

Our annual outlook on how the core spectroscopy techniques (molecular, atomic, and mass spectrometry) will fare in 2013 based on the results from last year's data.

In retrospect, 2012 was a major disappointment for the spectroscopy instrument market. In 2011, economic problems did little to halt laboratory purchasing plans, and we hoped that 2012 would show the same solid growth we had seen in 2010 and 2011. Unfortunately, it did not happen that way. During 2012, economic difficulties, especially in Europe, but also in the United States and Japan, had a major impact on prospects for the spectroscopy instrumentation industry. China, India, and Brazil — once the industry's saving grace — experienced a slowdown and thus contributed to lackluster sales. Some of the gloom was the result of political wrangling in the United States and uncertainty regarding negotiations over tax hikes and budget cuts, including the so-called fiscal cliff, caused corporate management to put expansion plans on hold. Likewise, austerity measures in Europe, a threatened euro, and recessions cascading from one country to another took their toll.

Spectroscopy is a key sector of the analytical and life-science instrument industry. For many years, the overall instrument industry and the spectroscopy segment in particular have proved to be quite resilient while providing scientists the tools they need for a vast array of applications in every conceivable industry. Although we are no longer seeing the double-digit growth of the 1990s, growth has been fairly steady for the last decade, averaging around 6% annually. Yet changing global economic conditions and governmental actions have had their effect.

As 2012 unfolded, the economic news became darker and darker. The actual economic downturn deepened when corporations and governments failed to make investments and added to the general economic uncertainty of the times. In January 2013, the International Monetary Fund (IMF) cut its forecast of world growth based in part on a continuing sovereign debt crisis in Europe. Although world economic growth was 3.2% in 2012, it was predicted the global economy would only increase by 3.5% for 2013, weighed down by continuing problems in Europe. The IMF also expects the euro zone to contract 0.2% in 2013, instead of expanding by 0.2%. Developing economies, on the other hand, have slowed slightly, but will still outpace advanced economies. News releases of China's recent economic results were encouraging; many observers had worried that economy was headed for trouble, which would have had a negative impact on the instrument industry so dependent on that growing market.

After assessing these events and trends and reviewing various industry data for 2012 and the prospects for 2013, Strategic Directions International, Inc. (SDi), a consulting and market intelligence firm specializing in this market, has estimated the total worldwide market for analytical and life-science instrumentation revenues at $43.7 billion for 2012, an increase of only 2.4% from 2011. SDi now forecasts that the analytical and life-science instrument industry will perk up somewhat in 2013 at a rate of 3.6%. Revenue growth for the industry is expected to do much better in 2014 and exceed 5% that year.

Aftermarket purchases of products and services, including such items as consumables (especially chemicals), software updates, and accessories, has become an important aspect of the analytical and life-science instruments market. As the installed base of instruments grows and the market matures, the aftermarket becomes especially important. In fact, in selected technology areas the aftermarket is a very significant product segment that is growing faster than instrument system revenues and is often more profitable. It is also true that for some technologies, instrument systems (hardware) may actually be declining in unit sales while the aftermarket provides at least minimal growth. So it should be noted that all the revenue projections in this article include the total mix of revenue sources: instrument system sales, aftermarket offerings, and service.

The Overall Spectroscopy Market

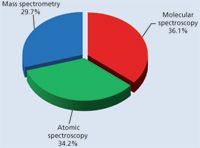

The spectroscopy market can be segmented into three distinct sectors: molecular spectroscopy, atomic spectroscopy, and mass spectrometry (MS) (Figure 1). The applications of the techniques included in each sector and their prospects differ significantly, especially within each sector. Worldwide revenue for all spectroscopy segments is estimated at about $10 billion for 2012, or about 22% of the entire laboratory analytical and life-science instrument market.

Figure 1: 2012 spectroscopy market by sector ($10 billion).

The overall spectroscopy market is estimated to have increased just 1.2% in 2012, a disappointing suboptimal performance primarily due to the economic uncertainty that existed throughout the year and finally impacted the market. SDi projects spectroscopy market growth in 2013 to remain in a slow-growth mode, but still expanding at a moderate rate of 3%. As with other analytical techniques, in 2011 the spectroscopy market was a beneficiary of the positive effects of a general return to global economic growth, and the last effects of government stimulus programs in several countries, especially in the United States, China, and Germany. Unfortunately, the situation reversed in 2012 as economic conditions worsened throughout the world, but especially in Europe. The pharmaceutical, biotechnology, and food industries still performed well, but most industrial markets, particularly metals, chemicals, and semiconductor manufacturing did poorly. In addition, government funding cutbacks took a toll on that sector, as well as on academia, which is dependent on government support. These were certainly lackluster markets for instrument suppliers. Some of these same developments will continue in 2013, preventing the spectroscopy market from making much of a comeback.

Molecular spectroscopy techniques accounted for more than 36% of the spectroscopy market in 2012, with several diverse techniques represented that address a wide range of applications in almost every industry category. Atomic spectroscopy is the second largest sector, at more than 34%, and mass spectrometry accounts for almost 30% of spectroscopy revenues. Please note that liquid chromatography (LC) and gas chromatography (GC) front-ends to mass spectrometers, and their associated aftermarket and service revenues, are not included in this analysis.

Initial system sales (hardware) represented about 69% of spectroscopy revenues in 2012. Aftermarket purchases of accessories, software, and consumables accounted for approximately 18% of revenues, which is less than other laboratory techniques but still significant. Service revenues for service contracts, on-call service, and spare parts combined for about 13% of the total market.

Molecular Spectroscopy

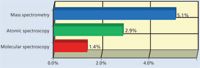

As predicted last year, the molecular spectroscopy market was not immune to a slow-growing economy, although the actual market decline of about 1% was an unexpected development. Several important segments of the market declined, including nuclear magnetic resonance (NMR) spectroscopy, the largest segment, as well as UV–vis and colorimetry. For 2013 the overall molecular spectroscopy market will increase modestly from 1% to 2% (Figure 2), held back by additional declines for NMR and colorimetry, albeit less so than for 2012. Most other segments of the market are expected to see fairly flat demand this year. Weakness in the academic sector and further cutbacks in government purchasing and funding will offset most of the improving picture from other industrial sectors in 2013, but an inevitable rebound should lead to high single-digit growth in 2014.

Figure 2: Estimated growth by spectroscopy sector for 2013.

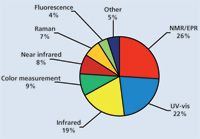

The NMR market, which has seen many years of double-digit growth and continues to be the largest segment of the molecular spectroscopy market (Figure 3), was hit by a substantial decline in 2012 as positive effects from stimulus spending gave way to government budget cuts, which also affected the academic market heavily. As governments continue to look to curtail spending in 2013, NMR demand is likely to decline somewhat in 2013. However, NMR is an extremely powerful technique, and a strong rebound is anticipated when the current period of government austerity fades, most likely in 2014.

Figure 3: The 2012 molecular spectroscopy market, broken down by technique.

The UV–vis market is large and extremely diverse, consisting of everything from simple, inexpensive photometric colorimeters used in water analysis test kits to high-end UV–vis–near infrared (NIR) systems used in the electronics and materials industry. The various subsegments of the UV–vis market are expected to see very flat growth in 2013, with the lone exception being microvolume UV–vis, which is largely driven by the biotechnology and related industries. A broad rebound across industries should lead to much stronger growth across all areas of the UV–vis market by 2014.

The infrared (IR) spectroscopy market will see the strongest growth of any molecular spectroscopy technique in 2013. Demand for portable IR instruments is helping to drive the market to some degree, with the oil and gas sector being a key to that area. The rise of terahertz spectroscopy, however, will be the biggest driver of the IR market in 2013. Although terahertz spectroscopy appears to be more suited to process and industrial applications, it is rapidly becoming a significant percentage of the infrared spectroscopy market.

After a modest decline in demand in 2012, demand for color analysis instrumentation should be approximately level in 2013. The big news in the market in 2012 was the acquisition of strong market leader X-Rite by Danaher Corporation.

Demand for NIR and Raman is expected to see similar growth rates in 2013. The strong connection of NIR to the agriculture sector is helping to insulate it somewhat from the cuts in government and academic spending that affect most other analytical technologies. In contrast, demand for Raman spectroscopy, which has seen very strong growth in recent years, is much more reliant on government and academic demand, resulting in a second consecutive year of low single-digit growth.

Demand for fluorescence and luminescence competes against microplate readers, which are included in another market segment. However, growth in industries such as environmental analysis is helping to maintain some level of expansion. Demand for ellipsometry is heavily tied to the semiconductor electronics industry, which is a highly cyclical market, and should result in a modest rebound by 2014.

A very large number of suppliers are involved in the design, manufacture, and sale of molecular spectroscopy instrumentation. Overall market share position, however, tends to be a function of dominance in particular product segments. Bruker continues to lead the molecular spectroscopy vendor share by a considerable margin as a result of its extremely strong position in the large NMR market coupled with its important role in IR spectroscopy. Thermo Scientific is a strong number two among molecular spectroscopy vendors because of its leading position in the UV–vis and IR markets, as well as its growing position in Raman spectroscopy. Agilent Technologies holds the number three position, based on its NMR business and several other molecular spectroscopy techniques, especially UV–vis. Danaher, with its strong role in instruments for water analysis, coupled with its recent acquisition of X-Rite, a dominant player in the color analysis market, has now moved into the number four market share position.

PerkinElmer remains a potent supplier of a variety of molecular spectroscopy instruments, especially UV-vis- and IR-based instruments. FOSS's dominance in NIR makes it one of the more significant molecular spectroscopy suppliers. Other important molecular spectroscopy suppliers include Shimadzu, JASCO, Horiba, and JEOL, all headquartered in Japan.

Atomic Spectroscopy

Atomic spectroscopy instruments generally provide information about the elemental composition of a sample, based on some form of light used to probe the sample. SDi identifies nine specific subtechnologies in this category, and each has its pluses and minuses for particular applications. The total market demand for atomic spectroscopy instruments is forecast to grow to nearly $3.5 billion in 2013 (Figure 4). This represents growth of about 3% for the year (Figure 2), an increase over the somewhat troubled market last year, which saw only very small gains. While some markets experienced small decreases last year, 2013 should usher in growth for all of the product segments in atomic spectroscopy.

Figure 4: Spectroscopy market by product segment ($ billion).

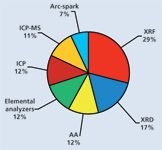

X-ray diffraction (XRD) is forecast to be the fastest growing technique, with growth approaching 5% for the year. XRD currently makes up about 17% of the atomic spectroscopy market (Figure 5). Unlike most atomic spectroscopy techniques, XRD is not primarily used for elemental composition; rather it is used to determine or identify molecular structures, or both. XRD has strong research applications in academic, government, and industrial laboratories in pharmaceuticals and biotechnology. Although budget constraints are affecting those markets, XRD continues to evolve as a technique with more automation and larger, faster detectors offering better performance, boosting both the price and demand for new systems.

Figure 5: The 2012 atomic spectroscopy market, broken down by technique.

The next most rapidly growing markets are inductively coupled plasma optical emission spectroscopy (ICP-OES) and ICP-MS. Both are standard elemental analysis techniques for environmental testing and many other uses. ICP-MS has the distinction of being the most sensitive technique, enabling detection of some trace elements at parts-per-quadrillion concentrations. ICP is a workhorse environmental technique, and ICP-MS is gaining ground as a result of increasingly strict environmental regulations as well as more interest in the effects of trace elements on health.

The remaining atomic spectroscopy techniques are forecast to experience growth only in the low single digits. Some techniques, like atomic absorbance (AA) are very standard techniques and generally do not provide much growth. Others, like arc/spark and X-ray fluorescence (XRF), are hindered by continuing uncertainties in the global economy and, in particular, weaknesses in the metals and consumer electronics markets. However, handheld XRF units continue to exhibit good growth as the applications for onsite analysis expand and the technique gains acceptance. Growth in this segment was less than 5% for 2012, but should approach 8% in 2013.

Looking further on to 2014, SDi expects the economic and industrial situation to improve markedly, and growth for all segments of atomic spectroscopy should accelerate through this year and into next year, when overall growth for the sector is forecast to exceed 5%.

Although no single vendor dominates this market, several have very strong positions in closely related technologies. PANalytical (part of Spectris plc), Bruker, Rigaku, and Thermo Scientific are strong in the X-ray technologies. Given that these are the largest markets, these four vendors are among the top six for all of atomic spectroscopy. Thermo Scientific is at the top of the list as a result of its broad performance in virtually all of these technologies, while the other three are more concentrated in certain portions of the atomic spectroscopy market. PerkinElmer and Agilent are major players in AA, ICP, and ICP-MS. LECO is a major player in the elemental analyzer market, and Spectro Analytical (Ametek) leads the arc/spark market. Hitachi was formerly a relatively minor player in AA and elemental analysis, but has recently become a more significant competitor following its acquisition of SII Nanotechnologies, which adds ICP, ICP-MS, and XRF to Hitachi's atomic spectroscopy portfolio. Other significant suppliers in this market include Horiba, Oxford Instruments, and GE Analytical Instruments.

Mass Spectrometry

Overall, MS growth is expected to be slightly above 5% in 2013 (Figure 2), which is somewhat stronger than the <4% growth seen in 2012, and well under the more typical pace of around 10% in recent history. With the lone exception of portable and in-field mass spectrometry, all categories of the technique are expected to see significantly better growth in 2013. Major overall trends in the market include increasing competition between the major vendors as they expand into more segments of the market, and significant moves by many of the leading vendors to position themselves to address the growing clinical analysis sector.

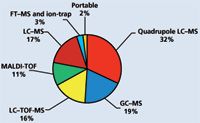

Quadrupole LC–MS, which includes both single-quadrupole and triple-quadrupole technologies, is the largest of the mass spectrometry categories (Figure 6), and will soon eclipse the $1 billion mark in annual sales. The strong pace of technological improvements in triple quadrupole sensitivity and performance continues to drive demand for high-end systems, while innovations trickle down rapidly to routine triple-quadrupole and single-quadrupole models as well. The entry of Shimadzu into the triple-quadrupole segment in 2011, followed by Bruker in 2012, has made the triple-quadrupole LC–MS area extremely competitive, with all six of the major mass spectrometer system suppliers now involved.

Figure 6: 2012 mass spectometry market by technique.

Single-quadrupole instruments dominate the installed base for GC–MS systems, and provide a very strong driver for replacement sales. However, most of the near-term growth in GC–MS is expected to come from the development of demand for triple-quadrupole GC–MS models, because this type of system is rapidly becoming a more routine analytical tool. The number of major system suppliers in the triple-quadrupole segment has been doubled by the relaunch of the former Varian business by Bruker and the entrance of Shimadzu into this segment. Another stimulus to growth of the GC–MS market has been the development of a commercial quadrupole time-of-flight (QTOF) GC–MS system by Agilent, which is helping to drive the smaller GC–TOF-MS portion of the market. Improvements in other GC–MS technologies are beginning to minimize many of the advantages of ion-trap technology, which is expected to see flat to slightly declining demand for the foreseeable future.

Fourier transform-ion cyclotron resonance-MS (FT-ICR-MS) systems, which are nearly all configured as LC–MS systems, have been grouped with ion-trap LC–MS systems because they both are based on various types of ion-trap designs. Although ion-trap LC–MS is still the larger percentage of the market segment, the return to double-digit growth for FT-ICR-MS is what will drive demand in 2013 (Table I). With the discontinuation of Agilent's high-end FT-ICR-MS business, and a minimal presence by Thermo Scientific, Bruker is becoming the only major supplier of such systems.

Table I: Spectroscopy product growth prospects for 2013

Thermo Scientific focused its efforts in this area on its Orbitrap-based FT-ICR-MS instruments, which are proving to be quite popular, despite facing intense competition from the QTOF LC–MS systems of other vendors. Demand for ion-trap LC–MS is expected to see fairly slow growth as end users continue to shift away from conventional designs in favor of linear and other, more novel, ion-trap LC–MS designs.

The vast majority of demand for LC–TOF-MS comes from QTOF systems, and is expected to see the strongest growth of all MS technologies in 2013. Most, if not all, of the major QTOF vendors have continued to make significant performance improvements annually, which has helped drive double-digit growth in most years. There has been considerably less developmental focus on LC–TOF-MS development, as the configuration does not allow for the use of most ion fragmentation techniques, and therefore growth in demand should continue to be much more modest.

Demand for MALDI-TOF-MS should be in the mid-single-digits in 2013, and likely stronger beyond that, as vendors, end users, and regulators are developing effective pathways to implementation of mass spectrometry in clinical analyses. Magnetic sector demand is largely relegated to niche applications and will continue to gradually wane. Demand for portable and in-field MS is dominated by government, which is likely to take a significant hit in demand in 2013 before bouncing back.

During the last few years, portable MS has developed into a major segment of the market, with advances in miniaturization and ruggedness, and growing interest in instrumentation focused on security. Unfortunately, a good portion of the demand for portable MS is reliant on government spending, especially for military applications. Government spending cutbacks have, therefore, affected the growth of portable MS, which is now slightly negative, but should rebound in 2014.

Industry consolidation and heightened competition during the last few years has concentrated market shares with six firms now accounting for more than 85% of the MS market. AB Sciex is the market leader based on its dominance in quadrupole LC–MS coupled with strong TOF-MS offerings. The other major mass spectrometry vendors include Thermo Scientific, Agilent Technologies, Waters, Bruker, and Shimadzu, all of which offer a number of mass spectrometry techniques. Although not as broad-based, suppliers such as PerkinElmer in GC–MS, LECO in GC–TOF-MS and LC–TOF-MS, and JEOL in magnetic sector technology, maintain important positions in their respective areas of emphasis.

The Spectroscopy Market Needs a Shot in the Arm

Innovation in the spectroscopy market has been a positive force in driving market demand for many years. The innovation comes from a push-pull effect between instrument companies and scientists that typically results in instruments being developed that meet the needs of the scientific community. Of course, new and improved instruments must be available to stimulate buyer interest, and business requirements and budgets must be sufficient to justify instrument purchases. Unfortunately, none of these elements has been particularly vibrant in recent years, and the near-term prospects are only slightly more promising.

Innovation has slowed during these uncertain economic times as instrument companies have moderated new product introductions and the research and development efforts needed. Likewise, resources for sales and marketing efforts have also suffered as suppliers have adjusted to poor market conditions. Clearly, both of these activities need to accelerate to provide the incentive for laboratories to consider new instrument acquisitions.

Spectroscopy techniques also have been found to be convenient solutions for analytical challenges for new and more demanding applications, especially when instruments are developed in more usable configurations and with superior performance capabilities. Handheld and portable instruments have helped to bring analytical techniques to the sample (rather than the other way around), so field analysis has become more viable. Field analysis is invaluable to scientists and technicians endeavoring to identify hazardous substances in water, soil, clothing, and food. Likewise, handheld and portable spectroscopy technologies have been found to be indispensable for security and defense, drug identification, food inspection, and environmental monitoring.

Although there are major concerns regarding the markets in Europe, other geographic markets are generally improving and should take up the slack. The U.S. economy is perking up and disagreements about spending and taxes may be headed for resolution, which would reduce economic uncertainty. Japan is also moving into an expansionary mode to revive its economy and China appears to continue to be the growth engine for the spectroscopy industry. Important end markets such as the pharmaceutical industry, biotechnology, and agriculture and food will be leading demand sectors in the coming months. Most applied markets like chemicals, metals, and electronics will lag, but still continue to contribute to an increase in overall demand. But perhaps the most important sectors that must rebound are governmental and academia markets, both linked and critical to spectroscopy market growth potential.

The various types of spectroscopy techniques address different analysis challenges and collectively represent a set of solutions available to scientists. And while many instruments compete, invariably a particular instrument does the job better than others. So this diversity and scope contributes to spectroscopy's continued importance and presence in laboratories around the world. But this diversity has also minimized its vulnerability to sectors of the economy most affected during economic downturns as the various techniques address applications in markets like the healthcare and pharmaceutical industries that are driven by different dynamics than the overall economy.

So throughout the next several months, we expect to see a number of new product introductions timed to improvements in economic conditions. The efforts of spectroscopy instrument manufacturers will undoubtedly stimulate demand and address the technical challenges faced by scientists that only get more difficult with each passing year.

Lawrence S. Schmid is the president and chief executive officer at Strategic Directions International, Inc. in Los Angeles, California. Direct correspondence to: lschmid@strategic-directions.com

LIBS Illuminates the Hidden Health Risks of Indoor Welding and Soldering

April 23rd 2025A new dual-spectroscopy approach reveals real-time pollution threats in indoor workspaces. Chinese researchers have pioneered the use of laser-induced breakdown spectroscopy (LIBS) and aerosol mass spectrometry to uncover and monitor harmful heavy metal and dust emissions from soldering and welding in real-time. These complementary tools offer a fast, accurate means to evaluate air quality threats in industrial and indoor environments—where people spend most of their time.

NIR Spectroscopy Explored as Sustainable Approach to Detecting Bovine Mastitis

April 23rd 2025A new study published in Applied Food Research demonstrates that near-infrared spectroscopy (NIRS) can effectively detect subclinical bovine mastitis in milk, offering a fast, non-invasive method to guide targeted antibiotic treatment and support sustainable dairy practices.